The EU taxonomy for sustainable activities was officially published in June 2020. It is the first official document to define and classify sustainable economic activities across Europe. Six months later, the People’s Bank of China (PBOC), National Development and Reform Commission (NDRC), and China Securities Regulatory Commission (CSRC) published a new edition of the China Green Bond Endorsed Project Catalogue (the Catalogue). This is the first time that all three Chinese regulatory authorities have reached an agreement on the classification and definition of green projects. Both of these documents – the EU taxonomy and the Catalogue – will act as important reference points for green finance institutions and investors in Europe and China. This article briefly summarises the content and impact of the documents.

The EU taxonomy for sustainable activities

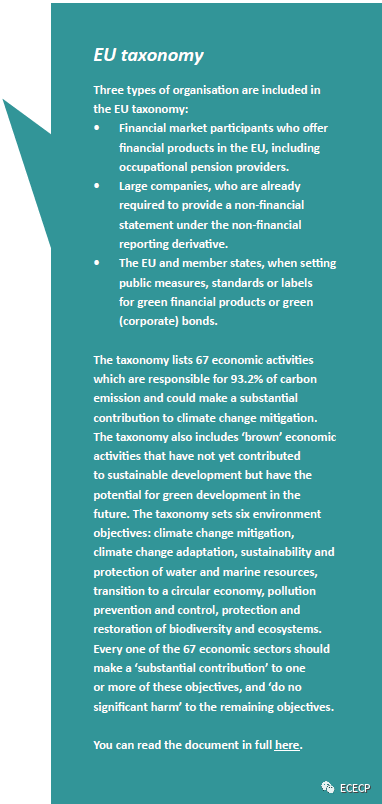

The EU taxonomy is the world’s first official system to define and classify a list of environmentally sustainable economic activities. The publication and implementation of the EU taxonomy provides clear guidelines as to what can be classified as ‘green’.

The aim is to orientate and improve the flow of money towards more sustainable activities. It is widely believed that this classification system will have a profound impact on the green economy worldwide.

Before the introduction of a complete classification system, ‘green’ decisions from investors, fundraisers and borrowers were mainly driven by intuition. Investors tend to be cautious with their money and fundraisers have been known to practise ‘greenwashing’ – where they present an economic activity as green when it is nothing of the kind.

The result is that it is extremely difficult for green projects to get financing, and green funds are less effective. The EU taxonomy provides a scientific classification that defines ‘green’ activities and provides a standardised information disclosure process for fundraisers and borrowers. Investors and fundraisers can identify green projects with a high degree of reliability and accuracy, and ‘greenwashing’ becomes harder to achieve. This is set to improve the effectiveness of green funds and increase the flow of money into industries that are making solid contributions to sustainable development.

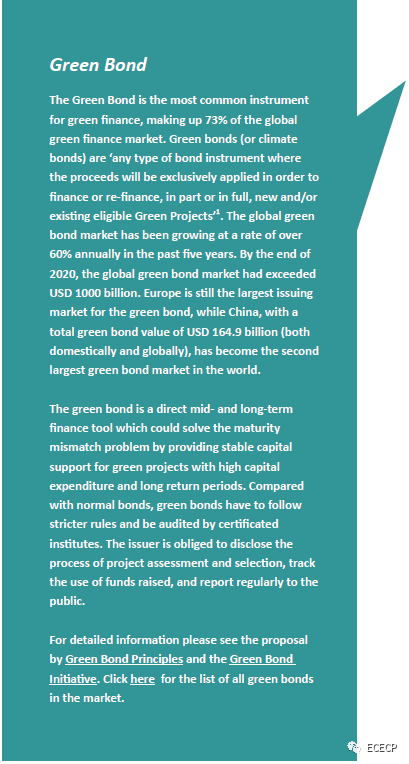

The EU taxonomy is designed to provide a basic understanding of what qualifies as green, and offer guidance on all forms of green finance tools. There are four mainstream green finance channels – green bonds, green loans, through green private equity, and through listed companies. Among the four types of equities, the green bond is the most mature and sustainable finance product. ‘The intention is to start with green bond and to go way beyond that,’ states Mathias Lund Larsen, senior consultant at the International Institute of GreenFinance (IIGF) and PhD fellow at Copenhagen Business School. ‘Now the EU is also developing a green bond standard on the regulations around how to make a green bond, using the taxonomy as the baseline. Issuers for the normally non–transparent equities, such as green loans and private equities, now also have to follow the taxonomy, or otherwise no investors will pay attention.’

The EU taxonomy provides a clear disclosure procedure for the assessment of green finance projects that all investors and fundraisers in Europe must follow. Institutions and corporate entities that have listed ‘sustainable activities’ in their portfolios have to report annually and explain the portfolios’ alignment with the EU taxonomy, so that the investors and the public can compare the portfolios of different companies and gain more confidence.

The taxonomy improves the credibility of green projects and encourages investors and fundraisers to self–regulate. The disclosure procedures can only be a positive development for equities and institutions who monitor their funds effectively. Although the EU taxonomy only applies to European financial institutions, other countries and regions are likely to feel its impact. International companies that finance, operate or are listed in Europe are also obliged to follow the EU taxonomy. Moreover, other countries are likely to refer to the EU taxonomy when they create their own taxonomies. This could attract investors and make it easier for companies to raise financing if they follow the taxonomy even if they are not based in Europe. The result could be a convergence of green finance standards across the globe.

Just six months later, the 2021 edition of Green Bond Endorsed Project Catalogue was released in China. The Catalogue was first released by the PBOC in 2015, but it conflicted with other documents issued by NDRC and CSRC. However, the 2021 edition was released and endorsed jointly by PBOC, NDRC and CSRC, the three key regulation authorities, for the first time providing uniform regulation for China‘s green bond market.

The 2021 edition of the Catalogue classifies. Green activities according to six key areas of activity: energy conservation, pollution prevention and control, resource conservation and recycling, clean transportation, clean energy, ecological protection, and climate change adaptation. This classification approach is different to that of the EU taxonomy, but it has the potential to be a more effective reference for bond issuers as it offers a target–based approach.

The biggest innovation of the 2021 edition is that it converges with international standards.The 2015 edition conflicted with the EU taxonomy and other internationally recognised taxonomies on many controversial activities, including fossil fuels, clean coal, nuclear energy and so on. For example, clean coal would never appear in the EU taxonomy, but was included in the 2015 edition of the Catalogue. This is due to the different environmental targets of the two regions. The EU pays more attention to the overall effect of economic activities on climate change and the whole environmental system, while developing economies are more interested in pollution mitigation given their heavy reliance on fossil fuels.

A big step forward in the 2021 edition is the removal of clean coal from the Catalogue, which means that ‘China is rapidly moving its attention from pollution mitigation to climate change,’ according to Wenhong Xie, China program manager at the CBI.

This is set to have a positive influence on the attitude of international investors to the Chinese market, which is currently dominated by domestic investors. Moreover, the 2021 edition has added activities that have seen rapid growth in recent years, including green agriculture, sustainable buildings, unconventional water resources utilisation, and so on.

The ‘do no significant harm‘ principle was also introduced into the 2021 edition. Wenhong Xie believes that the main aim of the 2021 edition is to improve corporate awareness of sustainability. Although the 2021 edition also helps screen out greenwashing from the market, the main purpose appears to be more of a discovery process – to help corporate entities to become aware of the green assets and green investments on their balance sheets, which previously failed to be identified because of the lack of a clear definition and classification. With the release of the 2021edition, the market size, liquidity and transparency of green bonds are also expected to grow, and this could eventually bring more opportunities into the climate mitigation industry.

Right now, China and the EU are working closely together to develop a universal taxonomy under the International Platform on Sustainable Finance (IPSF) in order to bring more investment into the climate industry worldwide.

The taxonomy and the Catalogue share similar principles and targets, but disagreements still exist. In terms of content, the EU taxonomy provides a more detailed definition of specific economic activities and industries, and also includes prospective industries, such as the digital and information industry. Moreover, the activities in the Catalogue have not been aligned and standardised to conform to the Classification by the National Bureau of Statistics, whereas the EU taxonomy is based on the Statistical Classification of Economic Activities in the European Community (NACE), which is widely used for data collection and can be more easily promoted globally.

In terms of approach, China is presenting itself as a policy pioneer, based on a top–down approach, while the EU is presenting itself as a setter of standards, based on a bottom up approach. The Catalogue includes compulsory measures, such as fines and punishments, to encourage the institutions to obey, while the EU taxonomy is still voluntary rather than mandatory. This does not alter the fact that green financial instruments tend to be self–labelled and are subjectively evaluated by issuers and investors. Despite these differences, a process of institutional convergence has begun.

According to Mathias Lund Larsen, ‘the first step in the process of institutional convergence happens when China pioneers green finance policies and moves them into the realm of what it is. The second step takes place when EU develops policies in those areas that become global standards.’ He believes that while convergence takes place at the policy level, it does not happen at the level of the underlying capitalist models. It may signify the importance of an activist state in climate change, making the current global competition between capitalist entities an advantage as systems complement and compete with each other, even as they collaborate.

Conclusion

As two of the biggest green finance markets in the world, the EU and China are taking the lead when it comes to green finance regulation. By providing a well–defined classification of green activities and a clear investment disclosure process, the EU taxonomy and the China Green Bond Endorsed Project Catalogue have created standard and transparent markets for market participants in the EU and China. Although their actual effect is as yet unknown, the publication of the taxonomy and the Catalogue undoubtedly provide important guidance and motivation for other countries and regions.

With the implementation and convergence of the taxonomy and the Catalogue, green classification is now set to be mapped and established in more countries and regions. Many hope that this will result in an active, uniform, and well structured global green finance market.

By Brian Yang

ECECP Junior Postgraduate Fellow